Nekateri IPO-ji so bili odlična priložnost za zaslužek, drugi pa niti ne.

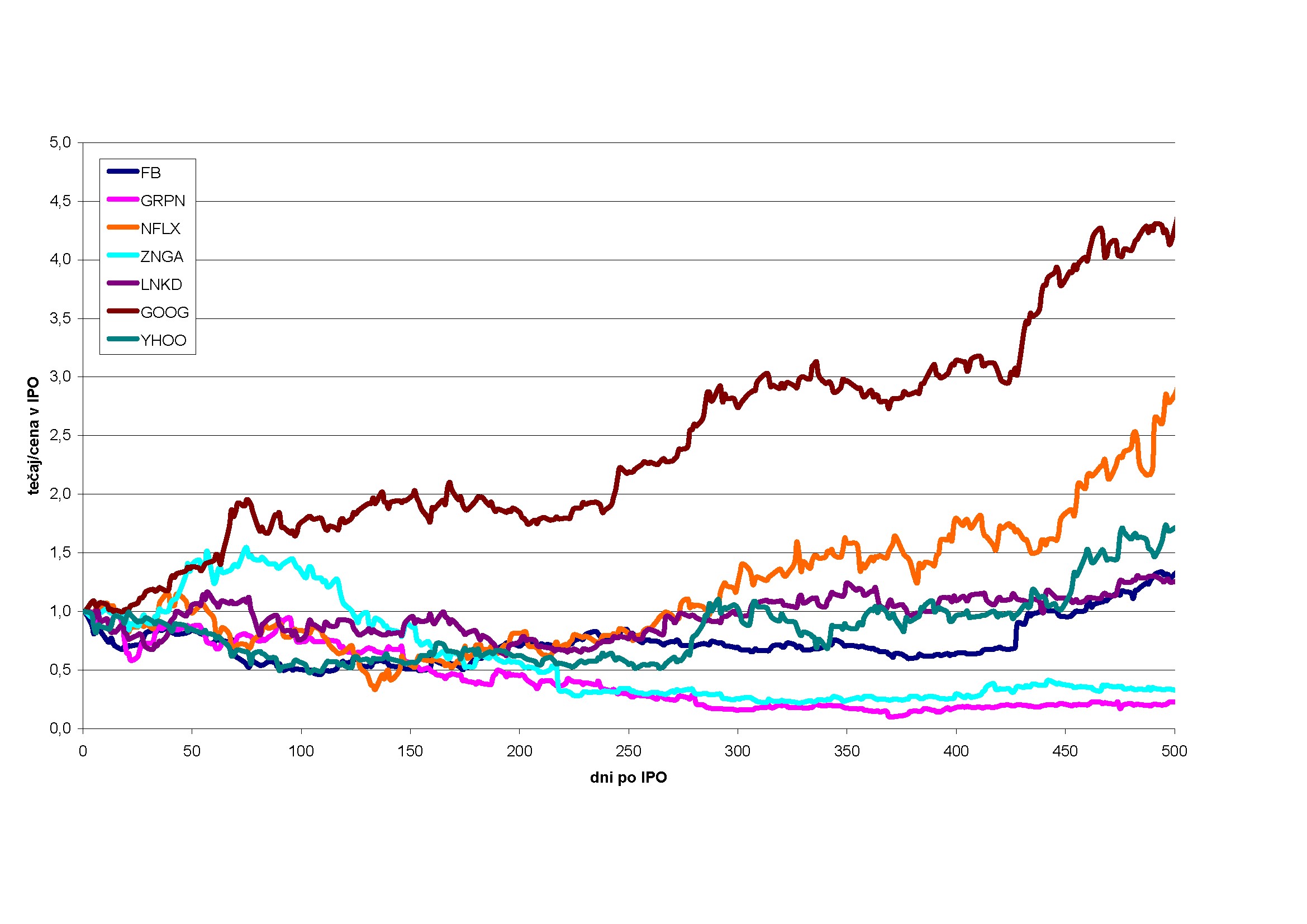

To je za podjetje, ki še nikoli v zgodovini ni poslovalo z dobičkom, veliko. Facebook, ki je sicer danes vreden več kot je bil na dan IPO-ja, se je ob začetku kotacije klavrno sesul, dodatne preglavice pa so povzročale tudi tehnične težave. Twitter pa je primerjalno gledano na Facebook še dražji, saj je razmerje med ceno delnice in prihodki od prodaje (P/S) 11,8. Količnik P/E pa je za Twitter negativen, saj podjetje še nikoli v zgodovini ni ustarilo dobička. Facebook ga pred IPO-jem namreč je. Precej slabo sta se po svojih IPO-jih odrezala tudi LinkedIn in Groupon, ki sta prav tako pristala bistveno nižje od cen v javni ponudbi.

15.30 Trg se je normalno odprl, z delnicami Twitterja se trgovanje še ni pričelo.

15.50 Še vedno poteka usklajevanje o otvoritveni ceni. Bloomberg neuradno piše, da sta na nakupni strani naročili za 10 milijonov delnic po 30 dolarjev in za tri milijone delnic po 40 dolarjev. (Trgovanje s Facebookom se je prvi dan začelo s peturno zamudo.)

16.00 S Twitterjem naj bi se začelo trgovati po tečaju 42-46 dolarjev.

16.25 Interval se zlagoma oži, trenutno se napovedi gibljejo v razponu 45-46 dolarjev.

16.26 Neposredni prenos s trgovalnega parketa lahko gledate tukaj.

16.40 Vrvež na NYSE je nekoliko potihnil, upadel je tudi promet z ostalimi delnicami. Vsi čakajo, kdaj se začelo trgovati bo Twitterjem. To se lahko zgodi tudi šele čez nekaj ur.

16.43 Razpon se je skrčil na 45,5-46,5 dolarjev.

16.45 Verjetno marsikoga zanima, zakaj delnice prvi dan po IPO ne začnejo kotirati ob odprtju trga. Otvoritvene cene se izračunajo v avkcijskem načinu. Vsako prodajno naročilo (če ni tržno) namreč določa minimalno ceno, po kateri se bo izvedlo, hkrati pa vsako nakupno naročilo določa maksimalno ceno. Otvoritvena cena se določi tako, da se izvede največ poslov. Če bi na tak način začeli trgovati s Twitterjem takoj po odprtju borze, bi zaradi neuravnotežene ponudbe in povpraševanja tečaj divje nihal. Zato se nekoliko počaka, da se knjiga naročil popolni in umiri.

16.50 Razpon je sedaj 45,00-45,25 dolarjev.

16.51 Trgovanje s Twitterjem se je začelo pri 45,10 dolarja.

16.52 Otvoritveni tečaj Twitterja je za 75 odstotkov višji od cene v IPO. To je za kupce v IPO odlično, za podjetje pa to pomeni, da je na trgu pustilo skoraj polovico kapitala, ker se je očitno prodalo prepoceni. Po novem vrednotenje je celoten Twitter težak 32 milijard dolarjev, kar je desetkrat več od Krke.

16.55 Tečaj Twitterja je narasel na 47 dolarjev (+80 odstotkov na IPO).

17.00 Po aktualnih tečajih je Twitter najdražje tehnološko podjetje v zgodovini, merjeno glede na prihodke, saj dobička tako ali tako nima.

17.35 Twitterjev tečaj se je malo po 17. uri dotaknil meje 50 dolarjev, potem pa je delnica izgubila 10 odstotkov. Sedaj se je ustalila med 45 in 46 dolarji.

18.00 Ustanovitelji in zgodnji vlagatelji sicer ob IPO-jih običajno ne smejo prodati vse svoje zaloge delnic niti nimajo razloga, da bi to hoteli, a vseeno vsaj na papirju tisti dan tudi formalno precej obogatijo. Soustanovitelj Evan Williams ima v lasti 10 odstotkov Twitterja, torej je njegovo premoženje zraslo za okoli tri milijarde dolarjev. Jack Dorsey, izvršni predsednik, ima v lasti 23 milijonov delnic in je pravkar postal premožen - ima okroglo milijardo premoženja v Twitterju. Dick Costolo, izvršni direktor, ima 7,5 milijona delnic oziroma tretjino milijarde dolarjev. To so le najpremožnejši, številni drugi posamezniki in zgodnji vlagatelji (skladi) so pridelali lep plus.